- /

Understanding Maximum Loan Concessions for VA, FHA, and Conventional Mortgages

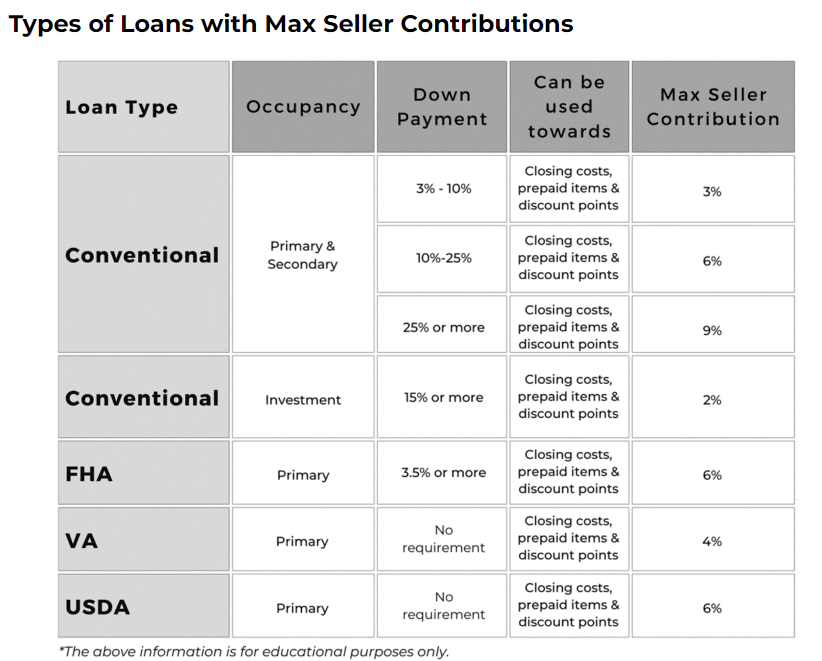

When purchasing a home, buyers often encounter various types of mortgages: VA, FHA, and Conventional. Each of these loans comes with specific guidelines and limits on concessions that sellers or lenders can offer. Understanding these concessions is crucial for both buyers and sellers to ensure a smooth transaction. Let's dive into the details.

Table of Maximum Loan Concessions

|

Loan Type |

Maximum Concessions |

Coverage |

|

VA Loans |

4% of the loan amount |

- Prepaid closing costs |

|

FHA Loans |

6% of the sale price |

- Loan origination fees |

|

Conventional Loans |

- 3% if down payment is less than 10% |

- Closing costs |

Details

VA Loans: Designed for veterans, active-duty service members, and eligible surviving spouses, VA loans offer benefits like no down payment requirements and competitive interest rates. Seller concessions can be up to 4% of the loan amount and cover various costs, excluding the buyer's normal closing costs.

FHA Loans: Popular among first-time homebuyers and those with less-than-perfect credit, FHA loans are backed by the Federal Housing Administration. Sellers can contribute up to 6% of the sale price towards closing costs and prepaid expenses, ensuring the buyer's equity is not overly reduced.

Conventional Loans: Ideal for borrowers with good credit and stable income, Conventional loans are not backed by any government entity. The maximum concessions depend on the down payment amount, ranging from 3% to 9%, covering closing costs, points, and other financing concessions.

Conclusion

Understanding the limits on loan concessions is essential for making informed decisions in the home-buying process. VA loans allow up to 4% in concessions, FHA loans up to 6%, and Conventional loans vary based on the down payment amount. Being aware of these limits helps buyers and sellers negotiate effectively and ensures compliance with loan guidelines. Always consult with a mortgage professional to navigate these details and maximize the benefits of your mortgage choice.

By grasping the nuances of loan concessions for VA, FHA, and Conventional mortgages, you can better prepare for the financial aspects of purchasing a home, ultimately leading to a more seamless and beneficial transaction for all parties involved.